Market Size of Global Viral Vector Manufacturing Industry

| Study Period | 2021 - 2029 |

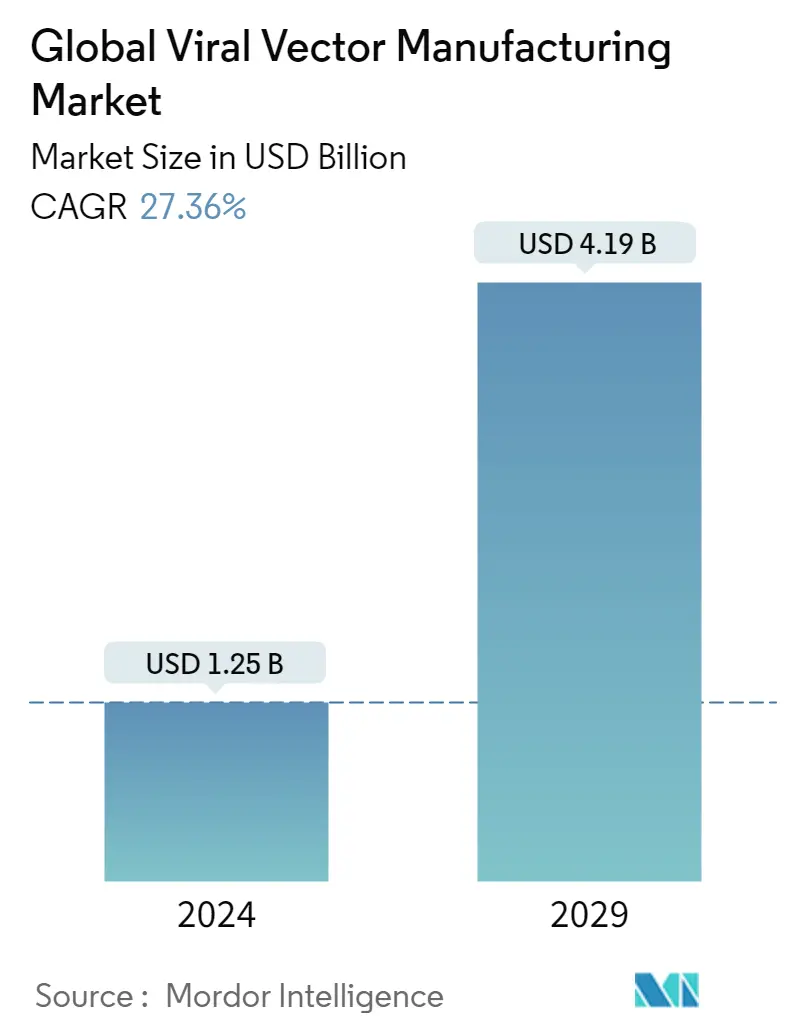

| Market Size (2024) | USD 1.25 Billion |

| Market Size (2029) | USD 4.19 Billion |

| CAGR (2024 - 2029) | 27.36 % |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

Major Players

*Disclaimer: Major Players sorted in no particular order |

Need a report that reflects how COVID-19 has impacted this market and its growth?

Viral Vector Manufacturing Market Analysis

The Global Viral Vector Manufacturing Market size is estimated at USD 1.25 billion in 2024, and is expected to reach USD 4.19 billion by 2029, growing at a CAGR of 27.36% during the forecast period (2024-2029).

The COVID-19 pandemic had underlined the importance of vaccine development for the global population, and it has had a positive impact on the growth of the viral vector manufacturing market. According to the WHO Global COVID-19 Vaccination - Strategic Vision for 2022, there are at least 17 vaccines in use. As of November 8, 2022, 12.88 billion doses were administered, and another 400 and more vaccine candidates were in clinical and preclinical development. Two viral vector vaccines have been authorized for emergency use in many countries for COVID-19, as of January 7, 2022, according to the Viral Vector Vaccines segment published by the Infectious Diseases Society of America. Moreover, various companies are launching their products and are involved in various partnerships, collaborations, and other developments which are expected to positively impact the market. For instance, in April 2020, AstraZeneca and Oxford University announced their partnership to develop a viral vectored vaccine utilizing a modified replication-deficient chimp adenovirus vector, ChAdOx1. Also, Janssen Biotech (Johnson & Johnson) has developed a viral vector vaccine utilizing a replication-incompetent human adenovirus vector and received approval from US FDA in February 2021, importance of viral vector manufacturing is increasing owing to the increasing research and developments occurring in current times.

The market is driven by the increasing prevalence of genetic disorders, cancer, and infectious diseases, the increasing number of clinical studies and availability of funding for gene therapy development, and potential applications in novel drug delivery approaches. For instance, as per the report published by the Foundation for Food & Agriculture Research in April 2022, African Swine Fever (ASF) has emerged as one of the highly contagious viruses that cause 100% mortality in swine. As of now, there is no commercially available vaccine to treat the disease. Therefore, to combat the disease, the Foundation for Food & Agricultural Research granted USD 145,000 to Genvax Technologies for developing a self-amplifying messenger RNA (saRNA) vaccine for African Swine Fever in association with the United States Department of Agriculture-Agricultural Research Services-Plum Island Animal Disease Center (USDA-ARS-PIADC). This prevalence of numerous infectious and viral diseases is motivating major companies to focus on viral vector product development and manufacturing.

Additionally, as the recombinant viral vectors are highly effective carriers of sequences encoding virus-disabling sequences, the appropriate and exact viral vectors usually need to be selected and adapted for application in the treatment of specific viral infections. Currently, there have been significant public and private sector initiatives are being taken for the development of viral vector vaccines, leading the key players to invest in capacity expansion for manufacturing activities. For example, in Augut 2022, Thermo Fisher opened a new manufacturing facility for viral vector production in Plainville, Massachusetts. The 300,000 square-foot-plant is opened with an aim to manufacture viral vectors, which are critical components in the development of gene therapies. Therefore, these related development activities by major players are also expected to boost the market's growth.

Government initiatives such as direct funding towards viral vector manufacture, which is increasing awareness, while the regulatory environment is getting streamlined via changes, such as prompt approval processes, are driving the studied market's growth. These aforementioned factors can propel the market for viral vector manufacturing and are expected to grow in the future. However, the high cost of gene therapies and challenges in viral vector manufacturing capacity can impact market growth negatively.

Viral Vector Manufacturing Industry Segmentation

As per the scope of this report, viral vectors represent one of the primary tools that can be used to deliver genetic material into cells. The viral vector manufacturing market is segmented by Type (Adenoviral Vectors, Adeno-associated Viral Vectors, Lentiviral Vectors, Retroviral Vectors, and Other Types), Disease (Cancer, Genetic Disorders, Infectious Diseases, and Other Diseases), Application (Gene Therapy and Vaccinology), and Geography (North America, Europe, Asia-Pacific, Middle East & Africa, and South America). The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD million) for the above segments.

| By Type | |

| Adenoviral Vectors | |

| Adeno-associated Viral Vectors | |

| Lentiviral Vectors | |

| Retroviral Vectors | |

| Other Types |

| By Disease | |

| Cancer | |

| Genetic Disorders | |

| Infectious Diseases | |

| Other Diseases |

| By Application | |

| Gene Therapy | |

| Vaccinology |

| Geography | ||||||||

| ||||||||

| ||||||||

| ||||||||

| ||||||||

|

Global Viral Vector Manufacturing Market Size Summary

The viral vector manufacturing market is poised for significant growth, driven by the increasing demand for innovative therapeutics, particularly in the fields of cancer treatment and vaccine development. The COVID-19 pandemic has underscored the critical role of viral vectors in vaccine production, with several viral vector-based vaccines receiving emergency use authorization globally. This has spurred numerous partnerships and collaborations among key industry players, enhancing the market's expansion. The market is further propelled by the rising prevalence of genetic disorders, cancer, and infectious diseases, alongside a surge in clinical studies and funding for gene therapy development. The development of novel drug delivery approaches and the growing interest in viral vector-based gene therapies for cancer treatment are also contributing to the market's robust growth trajectory.

North America currently leads the viral vector manufacturing market, with the United States playing a pivotal role due to its regulatory support and significant investments in research and development. The region's dominance is bolstered by the high adoption rate of new therapies and the presence of major industry players. Companies are actively expanding their facilities and investing in capacity enhancements to meet the growing demand for viral vectors. The market is moderately competitive, with both established and emerging companies vying for market share. Key players include Cognate BioServices Inc., Fujifilm Holdings Corporation, Merck KGaA, and Thermo Fisher Scientific Inc., among others. These developments, coupled with favorable government initiatives and a streamlined regulatory environment, are expected to sustain the market's growth momentum in the coming years.

Global Viral Vector Manufacturing Market Size - Table of Contents

-

1. MARKET DYNAMICS

-

1.1 Market Overview

-

1.2 Market Drivers

-

1.2.1 Rising Prevalence of Genetic Disorders, Cancer, and Infectious Diseases

-

1.2.2 Increasing Number of Clinical Studies and Availability of Funding for Gene Therapy Development

-

1.2.3 Potential Applications in Novel Drug Delivery Approaches

-

-

1.3 Market Restraints

-

1.3.1 High Cost of Gene Therapies

-

1.3.2 Challenges in Viral Vector Manufacturing Capacity

-

-

1.4 Porter's Five Forces Analysis

-

1.4.1 Threat of New Entrants

-

1.4.2 Bargaining Power of Buyers/Consumers

-

1.4.3 Bargaining Power of Suppliers

-

1.4.4 Threat of Substitute Products

-

1.4.5 Intensity of Competitive Rivalry

-

-

-

2. MARKET SEGMENTATION (Market Size by Value - USD million)

-

2.1 By Type

-

2.1.1 Adenoviral Vectors

-

2.1.2 Adeno-associated Viral Vectors

-

2.1.3 Lentiviral Vectors

-

2.1.4 Retroviral Vectors

-

2.1.5 Other Types

-

-

2.2 By Disease

-

2.2.1 Cancer

-

2.2.2 Genetic Disorders

-

2.2.3 Infectious Diseases

-

2.2.4 Other Diseases

-

-

2.3 By Application

-

2.3.1 Gene Therapy

-

2.3.2 Vaccinology

-

-

2.4 Geography

-

2.4.1 North America

-

2.4.1.1 United States

-

2.4.1.2 Canada

-

2.4.1.3 Mexico

-

-

2.4.2 Europe

-

2.4.2.1 Germany

-

2.4.2.2 United Kingdom

-

2.4.2.3 France

-

2.4.2.4 Italy

-

2.4.2.5 Spain

-

2.4.2.6 Rest of Europe

-

-

2.4.3 Asia-Pacific

-

2.4.3.1 China

-

2.4.3.2 Japan

-

2.4.3.3 India

-

2.4.3.4 Australia

-

2.4.3.5 South Korea

-

2.4.3.6 Rest of Asia-Pacific

-

-

2.4.4 Middle East & Africa

-

2.4.4.1 GCC

-

2.4.4.2 South Africa

-

2.4.4.3 Rest of Middle East & Africa

-

-

2.4.5 South America

-

2.4.5.1 Brazil

-

2.4.5.2 Argentina

-

2.4.5.3 Rest of South America

-

-

-

Global Viral Vector Manufacturing Market Size FAQs

How big is the Global Viral Vector Manufacturing Market?

The Global Viral Vector Manufacturing Market size is expected to reach USD 1.25 billion in 2024 and grow at a CAGR of 27.36% to reach USD 4.19 billion by 2029.

What is the current Global Viral Vector Manufacturing Market size?

In 2024, the Global Viral Vector Manufacturing Market size is expected to reach USD 1.25 billion.